Whether you use apps, spreadsheets or the envelope method, making a budget plan for you or your family can help you keep track of your spending.

If you’re looking for ways to bring your spending down, you might have already heard of “budget rules”. These are ways of managing your money by splitting up your expenses into three basic categories - needs, wants and savings - and deciding how much of your income you’ll spend on each.

There’s a lot of spending to keep track of in our daily lives. Especially if you’re managing bills and housing costs on top of day-to-day spending and treats like takeaway coffee.

If you find your spending difficult to keep track of, you’re not alone. According to the Financial Capability Survey, 39% of adults in the UK don’t feel confident managing their money.

This is where a budget rule can help!

What is a budget rule?

A budget rule is a simple way of managing your finances. By assigning every spend you make as either a need, a want or a savings contribution, you can limit how much of your income each type of spend should get.

Splitting your income (or household income) into these three categories can make budgeting feel a lot less overwhelming. It also helps you make sure you’re saving every month - something 34% of adults in the UK don’t do!

Popular budget rules

The two most popular budget rules are the 50/30/20 rule and the 70/20/10 rule. Here’s how they work:

Needs Wants Savings

50/30/20 budget rule 50% of your income 30% of your income 20% of your income

70/20/10 budget rule 70% of your income 20% of your income 10% of your income

These budget rules work for most people, but, as long as you stick to the three basic categories, you can come up with your own budget rule to suit your income and your expenses, we’ll explain how later on.

The 50/30/20 rule

Best for: those looking to save more money and cut down on expenses

This rule comes from a book called “All Your Worth: The Ultimate Lifetime Money Plan” which was published way back in 2005 and it’s still the most widely-used budget rule.

The 50/30/20 rules splits your monthly income in the following way:

- 50% (half) of your income should go to your necessary expenses

- 30% is set aside for your wants

- 20% goes towards building up your savings or making extra debt repayments.

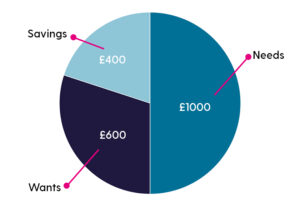

For example, this is how someone with an average income of £2,000 a month would split their income if they were following the 50/30/20 rule:

The 50/30/20 rule is designed to help you build up your savings faster and find ways to bring your necessary expenses down.

If you’re on a lower income or it’s simply not possible to reduce your expenses enough to fit that 50%, that’s okay – you can make your own budget rule or try the next one on the list.

The 70/20/10 rule

Best for: those with higher expenses or lower income

While the 50/30/20 budget is popular, many people can’t afford to cover all their expenses with just 50% of their income, especially if they live in a city where rent or mortgage payments are higher.

As the cost of living has gone up in recent years, a lot of people have instead built their monthly budgets around the 70/20/10 rule. With this budget method, 70% of your income covers your expenses, while 20% goes to your wants and 10% to your savings.

This is how someone with an average income of £2,000 a month would split their money to fit the 70/20/10 rule:

Leaving 70% of your income for expenses is likely to be more realistic for most people than 50%, especially when you consider the rise in energy bills and property costs.

Despite more money being set aside for needs, this budget rule still leaves you with 10% to put in your savings every month – which can add up to a lot more than you might think!

Your own budget rule

If neither the 50/30/20 rule nor the 70/20/10 rule fits your income, expenses and savings goals, you can always just make your own budget rule.

The important thing about any budget method is that it’s sustainable for you in the long-term, helps you work on your savings and leaves you with enough money to still have fun.

If you want to make your own budget rule, here’s a simple process to follow:

- Spend some time looking through your account statements and add up all your regular monthly expenses, as well as how much you tend to spend on groceries. Be honest with yourself!

- Once you have your “needs” amount, work out what percentage of your monthly income this is.

- Round it up to the nearest zero, so if your expenses add up to 53% you should set aside 60%. This will not only make it easier to think about, but it also gives you more breathing room for the food shop or a slightly higher bill that might surprise you. There’s no harm in having money leftover at the end of the month.

- Whatever’s left, whether it’s 50% or 20%, should be divided between “wants” and “savings” according to your priorities. If you’d like to reach your savings goals sooner, for example, you might want to cut down on your “wants” to boost your savings.

How to categorise your spending

Choosing which rule to follow will depend on how much of your spending tends to fall into each category. There are always a few things that could be either so it helps to plan how you will categorise your spending before you start.

Needs

Your needs category is where all your regular, necessary expenses go. This could include:

- Rent or mortgage payments

- Household and personal bills

- Necessary food and household items

- Minimum debt repayments (interest rather than capital)

- Insurance

- Transport

By choosing a rule to stick to, you can find ways to cut down on your necessary expenses to fit that rule even if you’re not there yet. You could look at switching to a different energy provider, find ways to save on your food shop and even move to a cheaper home.

This isn’t always possible, so it’s important that you choose a budget rule that’s realistic for you as you’ll be more likely to stick to it.

Wants

Your wants category is for any non-essential expenses – things that you want but can live without. This could be anything from takeaway dinners and new clothes to upgrading a household appliance.

Once you’ve figured out your needs category, you’ll be able to use it to help you decide if something you want is worth buying. If it takes you over your budget for your wants category then you might decide to do without.

Savings

The third category is for your savings. Your budget rule will help you decide how much you can comfortably put away every month, while still leaving enough for all your necessary expenses and fun purchases.

This category also includes debt repayments, on top of any minimum payments already in your “needs” category.

Sticking to your budget rule

The main benefit of a budget rule is that it takes the complicated process of building a monthly budget and makes it simple. No matter what budget rule you decide to follow, remember that the best budget is one you’ll actually stick to!

There are many tools and tricks out there to help stay on track.

- Download a budget tracking app. Take the time to fill out all your expenses, income and how much you want to put towards wants and savings. You could also turn on phone notifications so the app will let you know when you’re getting close to your budget limit in a specific category.

- Set up direct debits for your necessary expenses and your savings. This will take even more work off your shoulders and prevent you from forgetting to pay a bill or putting money in your savings.

- Split your account into pots or have different current accounts for needs, wants and savings. This can help make sure you don’t dip into money that should be set aside for bills or savings.

How can I start building up my savings?

Once you’ve decided on a budget rule and figured out how much you’ll be putting into your savings every month – the hard part is done!

Now you just need to decide where you’re going to save your money.

Your two main options are to save in cash or invest your money. Each option comes with its own pros and cons, but they differ in two main ways:

- how they make money

- how risky they are (to be clear, when we talk about risk, we mean the risk of ending up with less money than you started with).

Saving in cash makes money through interest, like your current account does. It’s the less risky option because you can’t lose money.

However your money will only grow as much as interest rates. If inflation (how much things cost) goes up by more than interest rates, your money will be able to buy less in the future.

Investing your money can be better in the long-term. You (hopefully) make money by it being invested, along with other investors’ money, in the stock market.

It has a higher potential to grow by more than cash savings, but it does come with the risk of losing money if your investments drop in value.

If you’d like to invest your savings long-term (for five years or longer), our Stocks and Shares ISA and Lifetime ISA both invest in stocks and shares funds and can be opened with monthly direct debits as low as £25!

Our Stocks and Shares ISA and Lifetime ISA invest in stocks and shares. This means they have good long-term growth potential, but the value of your investments could go down as well as up so you could end up with less money than you've put in.